Pet Food Industry Growth Supported by Expanding Health Awareness

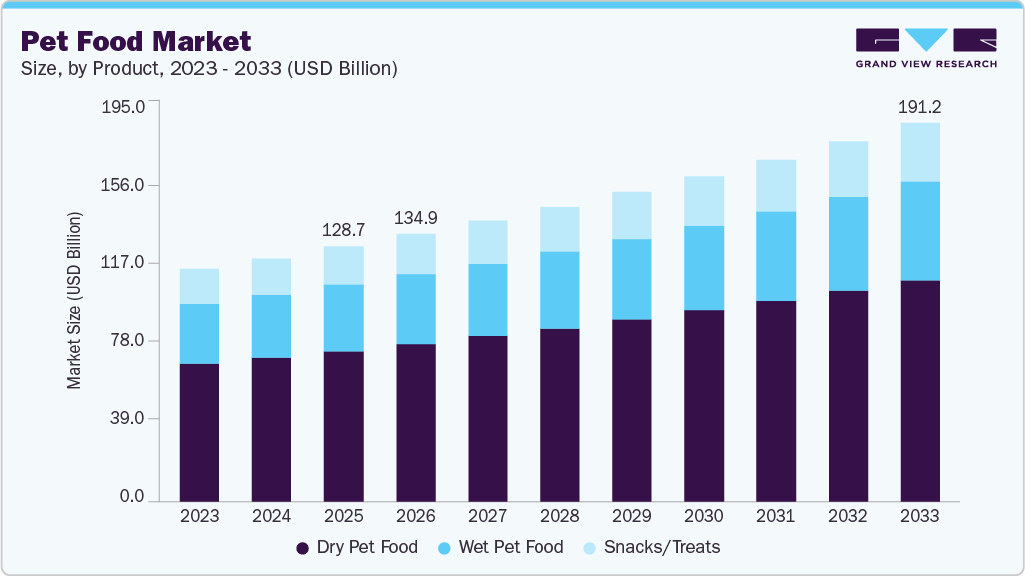

The pet food market continues to witness strong momentum as pet ownership rises steadily across developed and emerging economies. The global pet food market size was estimated at USD 128.73 billion in 2025 and is projected to reach USD 191.24 billion by 2033, growing at a CAGR of 5.1% from 2026 to 2033. Increasing consumer inclination toward pet adoption, coupled with growing awareness regarding pet nutrition, health, and wellness, is significantly contributing to market expansion. Pet owners are increasingly treating pets as family members, resulting in higher spending on premium, nutritious, and specialized food products designed to improve the overall well-being of pets. Manufacturers are responding to this evolving demand by introducing advanced formulations enriched with vitamins, minerals, proteins, and functional ingredients that support digestion, immunity, and overall performance in pets.

Growing awareness regarding the importance of balanced nutrition for animals is further accelerating demand across the pet care industry. Improvements in digestion, energy levels, coat quality, and the overall performance of pet animals owing to the consumption of nutritious food are expected to positively influence market growth over the forecast period. The increasing availability of customized pet diets, organic ingredients, and scientifically formulated products is also driving consumer interest globally. In addition, the growing popularity of premium pet food products, alongside rising disposable income and expanding e-commerce distribution channels, is creating lucrative opportunities for manufacturers and retailers. Companies are increasingly investing in innovation, sustainable ingredients, and advanced manufacturing technologies to cater to changing consumer preferences and strengthen their competitive positioning.

Key Market Trends & Insights

· North America accounted for the largest revenue share of 41.36% in 2025, supported by high pet ownership rates, strong consumer spending on pet care products, and increasing demand for premium nutrition solutions. The U.S. pet food market held the largest share of North America in 2025 due to the presence of established industry players, advanced retail infrastructure, and growing awareness regarding pet wellness and preventive healthcare.

· Based on product, the dry pet food segment dominated the market with a revenue share of over 59.10% in 2025. Dry pet food products continue to gain widespread popularity because of their affordability, convenience, longer shelf life, and ease of storage. These products are also preferred by consumers due to their ability to support dental health and provide balanced nutrition for pets.

· Based on pet type, the dogs segment held the largest revenue share of 60.75% in 2025. The increasing adoption of dogs as companion animals, along with rising expenditure on canine nutrition and healthcare, continues to support segment growth. Consumers are increasingly seeking premium dog food products formulated to address specific dietary requirements, age groups, and health conditions.

· Based on category, the traditional pet food segment held the largest revenue share of 86.18% in 2025. Traditional pet food products remain highly preferred among consumers due to their affordability, broad availability, and established consumer trust. However, rising interest in specialized and functional pet nutrition products is encouraging manufacturers to diversify their product portfolios.

Looking for more specific insights? Customize this report to suite your business needs

Key Companies & Market Share Insights

The competitive landscape of this market is moderately consolidated, with multinationals striving to meet high demand from large customers and the end-user base. Key industry participants are inclined to adopt new marketing strategies and use advanced technologies to strengthen their customer base and generate more revenue in the near future. In addition, companies are undertaking expansion, mergers, and acquisitions as part of their strategic initiatives. For example, in September 2023, Superlatus, Inc., a key food distribution and technology firm, merged with TRxADE HEALTH, Inc., and announced its expansion in the pet food industry with plant-based or vegan pet food treats.

Industry participants are inclined to invest heavily in research and technology to advance processes and develop new recipes, which are manufactured with varied and specialized ingredients. Key manufacturers are also focused on developing innovative formulas to offer diverse and high-quality food for pets and farm animals. Industry players also use raw materials to meet demand and regulatory criteria in both domestic and international markets.

Key Pet Food Companies:

· The J.M. Smucker Company

· Nestle Purina

· Mars, Incorporated

· LUPUS Alimentos

· Total Alimentos

· Hill’s Pet Nutrition, Inc.

· General Mills Inc.

· WellPet LLC

· The Hartz Mountain Corporation

· Simmons Foods Inc.

Grand View Research offers

· Focused market intelligence reports on specific geographies or high-growth segments.

· Extended forecast timelines for long-term planning.

· Competitor Benchmarking and Supply Chain Analysis

· Inclusion of regulatory and policy assessments.

· Inclusion of custom data models, KPIs, or applications unique to your business

· Specific high-impact Data Decks and Tables to support effective decision making

· And much more…

Looking for a report customized to your requirements? Explore our Custom Research Offering